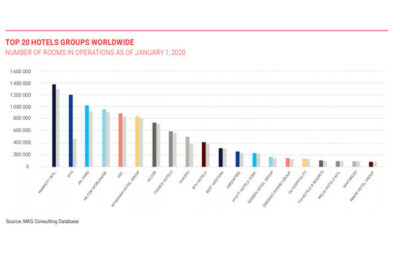

The American giant Marriott retains its title of global hospitality champion, as its room portfolio (1.4 million worldwide), profi tability ($1.1 billion adjusted EBITDA in 2020), and enterprise value (over $53 billion as at 1/1/2021) stand well above the pack.

A revolution is both a major change that disrupts the established order and a complete reversal that brings us back to the starting point: these two dynamics are exactly what the hospitality sector has gone through in recent months. The Covid-19 crisis has profoundly shaken up the fi nances and economic hierarchy of hotel groups, confi rming in particular the rise of certain Chinese players.

However, Western champions have almost managed to get back to their pre-covid valuation levels, and they are still ahead of the game in terms of financial strength. They have implemented different strategies to raise cash, and some have solid reserves preparing them for the future, where they will have to deal with formidable new challengers.

According to MKG Consulting, The American giant Marriott retains its title of global hospitality champion, as its room portfolio (1.4 million worldwide), profi tability ($1.1 billion adjusted EBITDA in 2020), and enterprise value (over $53 billion as at 1/1/2021) stand well above the pack. However, while Marriott unquestionably dominates this ranking, the group has seen its fi nancial valuation level decline slightly between January 2020 and June 2021 (-9%), a fact attributable to the fi nancial storm triggered by the global COVID-19 pandemic.

The 2nd financial champion of the hotel industry, Hilton, is also American. Its enterprise value, now approaching $45 billion (as of June 2021), is also justifi ed by a supply of more than one million rooms as of 2021. Its value is almost twice as high as the number three’s supply.

But behind these two uncontested leaders, the fi nancial hierarchy is changing fast. While most Western hotel groups have at best retained and more often slightly fell in value, Chinese operators such as Huazhu and Jin Jiang have seen their valuation surge in 2020 and H1 2021, even though they had not particularly suffered in 2019 from the earlier onset of the COVID epidemic on the Chinese market.

As a result, in the ranking of hotel groups by fi nancial value, Huazhu has risen to the third place, ahead of IHG and Accor. Indeed, while Accor lost a quarter of its enterprise value over the year 2020, Huazhu’s market capitalization increased by more than half.

This rise is partly due to the acquisition of Deutsche Hospitality by Huazhu and a considerable increase in the group’s supply (+22% compared to the previous year / +100K rooms) and various fi nancial factors detailed hereafter.

In the same vein, Jin Jiang rose to 5th place, overtaking the US-based Hyatt, Wyndham and Choice in 2020, and the French Accor in the fi rst half of 2021. As of June, its enterprise value is approaching $13billion.

II – What happened during the Covid crisis?

2020 and 2021 have been a rollercoaster to the hotel champions, which had to cope with one of the biggest challenges they ever faced.

The Covid-19 pandemic triggered a worldwide drop in hotel performance to historic lows. Meanwhile, the fi rst quarter of 2020 brought a sharp drop in stock market and valuation levels for hotel groups. Their fi nancial targets and analysts’ expectations had to be revised sharply downwards as lockdowns, travel bans and hotel closures were put in place to limit the spread of the virus.

However, while hotel performance was strongly affected throughout the year, stock markets in general and hotel group shares, in particular, recovered over the course of 2020, making it possible to cut losses. However, the timing and speed of this recovery seems to depend on their domestic market.

While the fall at the beginning of 2020 was more or less common to all hotel groups, the second half of the year marked a gradual recovery of the Chinese operators who then regained an advantage over their Western counterparts. Jin Jiang took the lead with a market capitalization that more than doubled (+127% from January 2020 marks), followed by Huazhu (+58%) and BTH Hotels (+31%). This early recovery can be explained by the timing of the health crisis and the

faster recovery of travel in China, especially since the country remains moderately exposed to demand from international customers. This positive momentum continued well into 2021, with Green Tree in turn initiating a bullish trend, while Jin Jiang extended its gains.

On the other side of the Atlantic, after experiencing a shock at the beginning of the pandemic, the Americans generally recovered in the end of 2020. Among them, Wyndham, Choice and Hilton have fully erased their losses and have even progressed in terms of market value over the past 18 months. However, in Q2 2021 their momentum began to wane. In Europe, however, the year was rather nightmarish from start to fi nish. While IHG was able to recover at the end of the year, Accor remained low, leading the French giant to be removed from the CAC40 index in September 2020. And in 2021, the signifi cant rebound of its value in Q1 was erased in Q2.

Overall, this year has been marked by the rise of Chinese groups, the resilience of American groups, and the relative loss of economic weight of European players. Will they manage to catch up in the second half of 2021?

III – Consequence: Staff reductions to control costs

In this particular market context, groups have unavoidably been forced to review their costs, to fi ght against a decline in their profi tability, and to reduce the speed at which they burned their cash. The crisis has therefore prompted hotel operators to make efforts to reduce the workforce at group level, i.e. at headquarters and in the hotels they own (very few today) or manage.

Among U.S. and European operators, the decline in headcount ranged from 10% to 37% depending on the group. Asmost of them have continued to expand their portfolio, this reduction is slightly more visible in terms of employees per room.

Overall, the staff-related savings achieved were signifi cant for all groups. They were particularly sizeable at Marriott, Wyndham and Hyatt, whereas Jin Jiang and IHG decided to limit the headcount cuts at headquarters. Accor, Hilton and Choice Hotels have adopted a balanced strategy between these two approaches.

IV – “Cash is king”: Who holds it?

Given the context, the performance and strength of groups are also measured by their cash fl ows, cash available and “cash burn”, a new fi nancial KPI that has made its unpleasant appearance in the hotel sector.

If the expression “cash is king” is true, some groups are ready for the future. This is the case for two groups in particular: Hilton and Accor, which stand out by hoarding particularly high levels of cash reserves.

In the case of Hilton, this is due to positive cash fl ows from fi nancing activities. Indeed, in response to the health crisis, the group decided to extend the maturities and reduce the interest rates of its outstanding debt, thus strengthening its liquidity position.

For its part, Accor shows encouraging levels of available cash, generated in a different way: by divestment fl ows, with in particular the sale of real estate assets of the Polish group Orbis for 1.067 billion euros, followed by those of Mövenpick in March 2020. The French group retained this strategy in the beginning of 2021 as it sold shares in the Chinese company Huazhu, which brought to the group a solid net capital gain.

Behind them but at a good distance, IHG also posted a good level of cash at the end of 2020, due to the cash infl ow from bond and commercial paper issuances under the Covid Corporate Financing Facility, a mechanism set up by the Bank of England to help companies in the context of the health crisis.

Hyatt, as well as Wyndham and Choice Hotels, to a lesser extent, have also pursued this strategy of raising cash through fi nancing deals. As pure franchisors, Wyndham and Choice currently have a much more limited cash position, but unlike some operators such as Accor or Hyatt, they have maintained positive cash fl ows from operations.

Finally, Huazhu and Marriott stand out for their particular strategies: the former drew on its reserves to close the Deutsche Hospitality buyout, and the latter maintained part of its initial dividend and share buyback program (in Q1 2020). It did so while recognizing as operating revenue $1.1 billion previously recorded as deferred from its Marriott Bonvoy loyalty program, and drawing $920 million in cash from agreements with the co-issuers of the credit cards associated with this loyalty program.

V – Value is relative

In terms of performance and profi tability, the ranking must also be put into perspective. Of course, the Covid-19 epidemic has caused an economic upheaval. As a result, 2019 EBITDA levels are more representative of the groups’ hierarchy than those of 2020, which are affected by the players’ business models (in particular the presence of owned, leased or managed hotels versus franchises) and by their different geographical exposures.

In terms of EBITDA per rooms operated, Hyatt leads the ranking, ahead of Marriott and Hilton. Accor, IHG and Huazhuare also well placed.

In terms of fi nancial valuation per room operated, four major players dominate the market with enterprise values standing between $35,000 and $45,000 per room: Hyatt, Hilton, Marriott and Huazhu.

Whereas most American operators lost value in recent months, Huazhu has made a step forward thanks to its surge in the stock market. It should be noted that the group, although Chinese, is listed on the New York Stock Exchange, unlike Jin Jiang, for example, number two in the world and much larger than its rival in terms of rooms but listed in Shanghai and Hong Kong.

Finally, OYO is not listed, but it raised funds in early 2021 (from Hindustan Ventures), valuing it at $9 billion. Like the other players in the sector, the group has therefore limited its decline in terms of post-pandemic valuation. However, in recent years it had achieved exponential growth at the cost of heavy fi nancial losses: in 2020, it had to slow down the pace of its cash burn, and saw its room portfolio shrink sharply.

As of mid-2021, enterprise values per room are therefore on the right track relative to 2020, and some operators have even managed to exceed pre-crisis levels.

V – Value captured elsewhere? Hotel groups vs. OTAs & digital players

However, let’s stake a step back and look at the broader picture: where does the value lie in the hospitality market? OTAs and digital players had already proved their weight in terms of valuation in recent years, and their stock market value bounced back quickly: in early 2021, Booking, for example, got back to the symbolic threshold of $100 billion valuation. And the year 2020 was also marked by a major event: on December 10, 2020, Airbnb went public through an IPO. Its rise in early 2021 enabled it to post a $80 billion valuation as of mid-2021. The result is that today, the major OTAs and peer-to-peer platforms total more than $250 billion, compared to just over $200 billion for the hotel champions.

If the stock markets have already erased the losses of 2020, the hotel champions still have a lot on their plate: to reactivate their operations, to restore their income statements and their post-COVID fi nances, and also to prepare for the future and get closer to these new travel champions.

Vicky is the co-founder of TravelDailyNews Media Network where she is the Editor-in Chief. She is also responsible for the daily operation and the financial policy. She holds a Bachelor's degree in Tourism Business Administration from the Technical University of Athens and a Master in Business Administration (MBA) from the University of Wales.

She has many years of both academic and industrial experience within the travel industry. She has written/edited numerous articles in various tourism magazines.