Of all shows originally scheduled to be held in the second quarter of 2022, 0.6% were postponed, 1.9% were cancelled and 97.5% were completed as scheduled. Excluding postponed events, the cancellation rate reached 2.0%, as indicated previously.

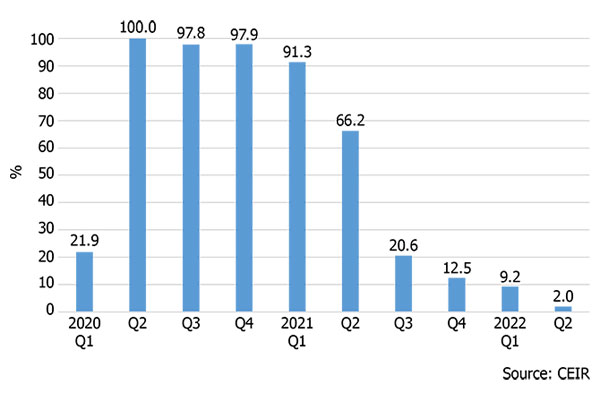

OXON HILL, MD. – The Center for Exhibition Industry Research (CEIR) announced, during its annual Predict Conference, that the U.S. business-to-business (B2B) exhibition industry improved significantly in Q2 2022 from the previous nine quarters. Cancellation rates for physical in-person events continue to drop, improving from 100.0% in Q2 2020 to 66.2% in Q2 2021, and rates sank to just 2.0% in Q2 2022.

Figure 1: B2B Exhibition Industry Cancellation Rate, %

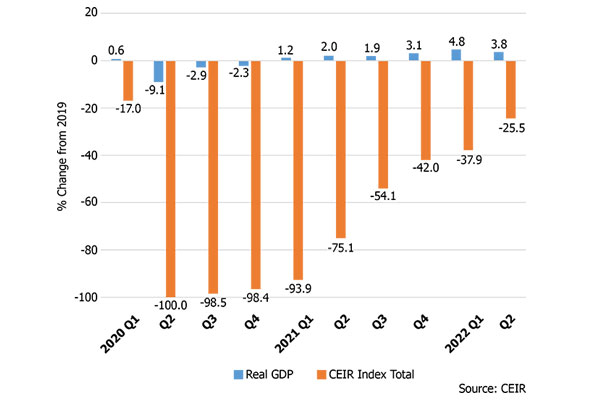

The drop in cancellations and the improvement in completed events boosted the Q2 2022 Index result. However, as expected, the CEIR Total Index – a measure of overall exhibition performance – remains in recovery, still falling below 2019 levels, with a result 25.5% lower than 2019 as shown in Figure 2 below. Nonetheless, this is a vast improvement compared to the past two years: a decline of 100.0% from 2019 in Q2 2020, 75.1% from 2019 in Q2 2021, and recently, 37.9% from 2019 in Q1 2022.

U.S. GDP and the CEIR Total Index

The performance of the U.S. economy was far better, registering a 3.8% increase in real (inflation-adjusted) GDP from Q2 2019 to Q2 2022. On a seasonally adjusted annual rate (SAAR) basis, real GDP in Q2 declined 0.6% from the previous quarter, on top of a decline of 1.6% SAAR in Q1. The drop in real GDP reflected primarily decreases in private inventory investment and, to a lesser extent, government spending at all levels and nonresidential fixed investment. These declines were partly offset by increases in personal consumption expenditures. Imports, which are a subtraction in the calculation of GDP, increased, but the trade deficit narrowed due to strong export gains. Had private inventory investment stayed the same, real GDP would have increased by 1.6% SAAR. The recent slower pace of inventory accumulation bodes well for GDP growth during the second half of the year, as many firms will place new orders rather than rely on existing stocks of merchandise. During the past two years, economic recovery has been led by strong spending on goods. However, the initially sluggish recovery in services industries recently has continued to pick up the pace. In Q2 2022, real spending on consumer services finally recovered pandemic losses, exceeding Q4 2019 spending levels by 0.9%. Other services industries are seeing similar improvements.

Figure 2: Real GDP vs. CEIR Total Index, Q1 2020-Q2 2022, % Change from 2019

Q2 2022 Exhibition Industry Performance

Of all shows originally scheduled to be held in the second quarter of 2022, 0.6% were postponed, 1.9% were cancelled and 97.5% were completed as scheduled. Excluding postponed events, the cancellation rate reached 2.0%, as indicated previously.

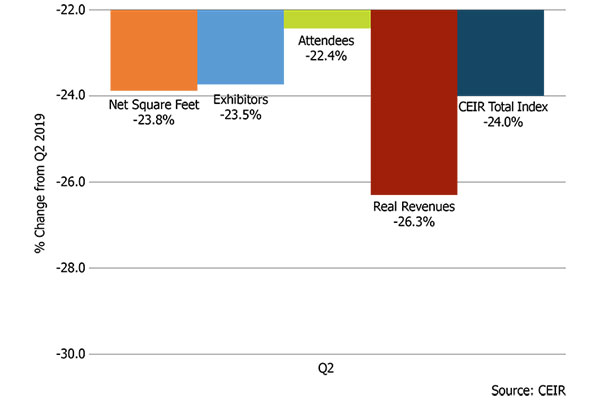

Figure 3 provides insights about events completed in Q2 2022, comparing performance to Q2 2019. Q2 2022 results speak to a continuing but choppy and uneven recovery that is underway. Still, the direction is positive, with the overall Index and specific metrics improving for the past five quarters. For the first time, Attendees is one of the strongest performing metrics. A good sign for the industry, as Attendees is a leading indicator. Among completed events, 10.5% have surpassed their pre-pandemic levels of the CEIR Total Index. Some organizers launched new shows, expanded existing shows to new locations or held them at a different time of the year. Excluding cancelled events, the Total Index for completed events in Q2 2022 dropped by 24.0% from 2019 (Figure 3), compared to a decline of 54.9% from 2019 in Q1 2021, 39.8% from 2019 in Q2 2021, 45.8% from 2019 in Q3 2021, 40.5% from 2019 in Q4 2021 and 31.6% from 2019 in Q1 2022. Real Revenues suffered the largest fall of 26.3%, followed by Net Square Feet (NSF) with a decline of 23.8%. Exhibitors tumbled 23.5%. Attendees in Q2 was the metric that contracted the least at 22.4% from Q2 2019.

Figure 3: Q2 2022 CEIR Metrics for the Overall Exhibition Industry Excluding Cancellations, % Change from Q2 2019

Insights on a Recession

There have been different views on whether the economy is in a recession and its implications on the exhibition industry. In CEIR’s view, two consecutive quarters of declines in real GDP does not mean the economy is in a recession, even though a well-known rule of thumb is that two or more consecutive quarters of declines in real GDP imply a recession. Both Q1 and Q2 real GDP came off from a sizzling level of real GDP growth in Q4 2021 (6.9% SAAR). On a year-over-year basis, real GDP increased 3.5% in Q1 and 1.7% in Q2. The recession arbiter, the National Bureau of Economic Research (NBER), declares a recession when there is “a significant decline in economic activity that is spread across the economy and lasts more than a few months.” The NBER’s determination of a recession “is based on a range of monthly measures of aggregate real economic activity published by the federal statistical agencies. These include real personal income less transfers, nonfarm payroll employment, employment as measured by the household survey, real personal consumption expenditures, wholesale-retail sales adjusted for price changes, and industrial production.”

In the U.S. Bureau of Economic Analysis’ (BEA) income side of the measurement for the economy, gross domestic income (GDI), U.S production expanded 1.8% SAAR in Q1 and 1.4% SAAR in Q2. Thus, there are unusually substantial discrepancies between the expenditure approach of GDP and income approach of GDI. Historically when that happened, GDP tended to be revised toward GDI. Averaging GDP and GDI, a proxy for the true state of the economy, the economic growth was relatively flat, increased by 0.1% SAAR in Q1 and 0.4% SAAR in Q2. It is very likely that the GDP in Q1 and Q2 might be revised up from a moderate decline to a modest increase.

The August payroll employment level increased by 315,000. Although lower than the enormous jump of 526,000 in July, it was still a solid gain. Furthermore, the employment increase spread across all key goods and services producing industries. The wide-spread employment increase clearly shows that the economy has not encountered “a significant decline in economic activity that is spread across the economy” and should expel the claim that the economy is in a recession. While recent corporate earnings reports were mixed, current economic data suggest continuing economic health that should support a moderate increase in economic activities during the second half of the year.

“Easing inflation and moderate economic growth ahead should lay a firm foundation of support to the B2B exhibition industry,” said CEIR Economist Dr. Allen Shaw, Chief Economist for Global Economic Consulting Associates, Inc. “The B2B exhibition cancellation rate should remain extremely low, and the performance of completed events will continue to improve.”

B2B Exhibitions Recovery

CEIR survey research and Index results indicate recovery of the industry will accelerate. CEIR Omnichannel Study results indicate strong intent to return in 2022, particularly on the exhibitor side but with slightly softer intent to return among attendees. The core values of the B2B exhibition channel motivate a return to participating, as COVID-19 ebbs.

“Despite Omicron at the outset of 2022 and variants that have followed, our industry presses on; many have held their events and have done so successfully and safely,” added CEIR CEO Cathy Breden, CMP-F, CAE, CEM. “CEIR research has documented an intent to return to face-to-face engagement at B2B exhibitions, and CEIR Index quarterly results show recovery is happening. With the safety measures implemented at large gatherings that have been held, and with a majority of the population vaccinated and boosted, the recovery of B2B exhibitions should continue in 2022.”

CEIR released the 2022 CEIR Index Report on 24 May, which analyzes the 2021 exhibition industry performance and provides an economic and exhibition industry outlook for the next three years. CEIR collects data directly from B2B exhibition organizers, who are encouraged to provide their show data by using the Event Performance Analyzer. In exchange for submitting data for a valid B2B exhibition, this tool enables an organizer to instantly see how an event’s performance compares to CEIR Index benchmarks at no cost. This tool was recently updated and provides users with a forecast for 2022. Data submission is strictly confidential. Click here for more information. The annual CEIR Index Report for their shows’ market sector will be provided to participating organizers at no cost.

Vicky is the co-founder of TravelDailyNews Media Network where she is the Editor-in Chief. She is also responsible for the daily operation and the financial policy. She holds a Bachelor's degree in Tourism Business Administration from the Technical University of Athens and a Master in Business Administration (MBA) from the University of Wales.

She has many years of both academic and industrial experience within the travel industry. She has written/edited numerous articles in various tourism magazines.