The CarTrawler global estimate forecasts 13% increase above 2017, with $64.8 billion of the total consisting of a la carte fee activity.

DUBLIN, IRELAND – IdeaWorksCompany and CarTrawler project airline ancillary revenue will reach $92.9 billion worldwide in 2018. The CarTrawler Worldwide Estimate of Ancillary Revenue represents a 312% increase from the 2010 figure of $22.6 billion, which was the first annual ancillary revenue estimate.

Earlier this year, CarTrawler and IdeaWorksCompany reported the ancillary revenue disclosed by 73 airlines for 2017. These statistics were applied to a larger list of 175 airlines to provide a truly global projection of ancillary revenue activity by the world’s airlines for 2018. The CarTrawler Worldwide Estimate of Ancillary Revenue marks the ninth year IdeaWorksCompany has prepared a projection of ancillary revenue activity.

Ancillary revenue is generated by activities and services that yield cashflow for airlines beyond the simple transportation of customers from A to B. This wide range of activities includes commissions gained from hotel bookings, the sale of frequent flyer miles to partners, and the provision of a la carte services ? providing more options for consumers and more profit for airlines.

“Nearly $93 billion in revenue indicates that good merchandisers are selling products desired by a vast number of customers. IATA estimates more than 4.3 billion travellers will depart on flights in 2018. Most of them now have the choice of paying a little extra for more comfort and convenience – thus providing airlines with a golden opportunity to build and strengthen their customer experience in the long-term,” said Aileen McCormack, Chief Commercial Officer at CarTrawler.

Analysis performed by IdeaWorksCompany during the past eight years reveals natural airline groupings (or categories) based upon a carrier’s ability to generate ancillary revenue. The “percentage of revenue” results associated with four defined categories have been applied to a worldwide compilation of operating revenue disclosed by 175 airlines(1).

PINAKAS

- Traditional Airlines. This represents a general category for the largest number of carriers. Ancillary revenue activity may consist of fees associated with excess or heavy bags, extra leg room seating, and partner activity for a frequent flyer program. The average percentage of revenue for 2018 remains unchanged at 6.7% from last year. Ancillary revenue innovation among global network carriers in Africa, Asia, the Middle East, and South America remains sluggish when compared to Europe and North America. Examples in the traditional airline category include Aerolineas Argentinas, Iberia, Japan Airlines, and Qatar Airways.

- Major US Airlines. US-based majors generate strong ancillary revenue through a combination of frequent flyer mileage sales and baggage fees. The percentage of revenue for this group remains unchanged from last year at 14.2%. The lack of growth was largely due to a reduction in pre-payments made by Chase Bank to United for its co-branded credit card program. Examples in this category include Alaska, Delta, and Southwest.

- Ancillary Revenue Champs. These carriers generate the highest activity as a percentage of operating revenue. The percentage of revenue achieved by this group jumped to 33.9% from 30.9% for 2017. The increase can be attributed to higher results from the big carriers in this category, and the addition of VivaAeroBus, Volotea, and WOW air to the list of disclosing carriers for 2018. Other examples in this category include: Allegiant, Pegasus, and Scoot.

- Low Cost Carriers. LCCs throughout the world typically rely upon a mix of a la carte activity to generate good levels of ancillary revenue. The percentage of revenue for this group increased to 12.4% from 11.8% for 2017. Low cost carriers include Air Arabia, JetBlue, SpiceJet, and Transavia.

Ancillary Champs and LCCs Lift Ancillary Revenue to New Heights

The ongoing growth of the global airline industry is responsible for 67% of the ancillary revenue increase for 2018. It’s said, a rising tide lifts all boats, and each of the four categories posted larger year-over-year results because of this. But within these numbers, the ancillary revenue champs and low cost carriers delivered a higher percentage of ancillary revenue against total airline revenue. The remaining 33% of the $10.7 billion annual increase was generated by a la carte-oriented airlines encouraging consumers to spend more on optional extras.

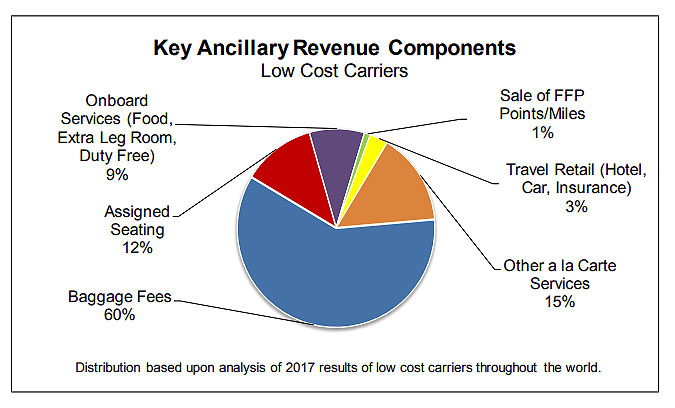

These carriers are the originators of ancillary revenue, and have always effectively managed the combination of low fares and a la carte features. Whereas traditional airlines offer a handful of optional extras, the true ancillary revenue evangelists manage a buffet of choices in the online booking path, through mobile apps, and solicitations sent after travel is booked. Of course, ancillary revenue champs and LCCs need to master the basics of bag fees and seat assignments. For a growing number of airlines, this is effectively accomplished through branded fares. This “good, better, and best” approach to bundling delivers exceptional results because half of consumers tend to upgrade to higher fares when branded fares are presented. The following pie chart displays the larger categories for a typical ancillary revenue savvy carrier.

Ancillary revenue champs and LCCs are simply better retailers and for traditional airlines that wish

to match these results, there is plenty of activity to observe. The following are some of the moves

these LCCs made during the last year to boost their ancillary revenue totals:

- AirAsia started tailoring dynamic pricing (such as bag fees) to individual customers at the end of 2017. These personalization methods improved the a la carte take rate by 6.7%.

- EasyJet’s invitation-only Flight Club recognition program has more than 50% of members flying 20 or more times a year, with just under 40% representing business or commuter customers. The program encourages these customers to remain loyal and spend more.

- JetBlue created a JetBlue Travel Products Group designed to tap more sales from non-air and travel retail categories with a focus on holiday packages.

- Jetstar introduced a FlexiBiz fare during 2017 which allows a large carry-on of 10 kg (22 pounds) without the usual checked bag. There’s no charge for same day flight changes and onboard food/drink is included.

- Ryanair encourages customers to book hotels via Ryanair Rooms by effectively returning its 10% commission in the form of travel credits, which customers can use to travel again on Ryanair in the next 6 months.

- Wizz Air had 64% of its digital interactions originating from mobile devices by the end of FY2018 with a mobile app that supports its a la carte and subscription initiatives.

Of course, the entire $92.9 billion annual result was not composed of these two categories alone. The flexibility of ancillary revenue allows any airline to generate revenue from a la carte options, commission-based travel retail, frequent flyer programs, and fare bundles. Many of the largest airlines in the world are embracing the practice of ancillary revenue.

Within the last year, the sale of basic economy style fares, which omit features such as checked bags and seat assignments, became prevalent among the carriers that fly transatlantic routes, as well as flights within North America and Europe. United disclosed during 2017 the lure to upgrade above basic economy went exceedingly well; 60% to 70% of passengers selected the higher priced standard product over basic economy when given a clear choice. IdeaWorksCompany anticipates the basic economy product design will spread throughout the world and will likely lift ancillary revenue activity for traditional airlines in Africa, Asia, the Middle East, and South America.

Ancillary revenue tops $21 per passenger for 2018

IATA predicts more than 4.3 billion passengers will spend $871 billion worldwide on air transport for 2018(2). Applying the global ancillary revenue estimate to IATA’s statistic yields a result of $21.32 per passenger. IATA also estimates the airline industry will spend $188 billion on fuel during 2018, which is up substantially from the 2017 level of $149 billion. Ancillary revenue now equals almost half of the industry’s annual fuel bill. All those individual sales of seat assignments, checked bags, and frequent flyer points provide a solid hedge against fuel prices.

Representing 10.7% of global airline revenue, ancillary revenue continues to contribute mightily to industry margins, which IATA predicts will be 6.8% for 2018 (earnings before interest and tax). It’s startling to recall that ancillary revenue as a percent of industry revenue was just 4.8% in 2010. Even the a la carte portion of today’s 10.7% rate (which removes the contribution of frequent flyer programs and commission-based activities) is a very meaningful 7.4% of total airline revenue. That figure has come a long way from the rate of 2.6% in 2010.

Economic fluctuations can quickly alter the health of the global airline industry and lead to higher fares. The results described in this annual estimate represent good news for airlines and consumers. The connection between ancillary revenue and financial health for airlines is now clear and is a solid component of the industry’s financial profile. Consumers too are learning to appreciate the a la carte choice as revenue-savvy airlines have become better shopkeepers.

Consumers will always reward companies that treat them honestly with fairly-priced products that provide what is promised.

(1) Operating revenue results were drawn from annual rankings in the July/August issue of Flight Airline Business. Additional sources were used, such as global alliance fact sheets and airline websites, to complete the list of 175 airlines. Adjustments were made to prevent duplicate reporting associated with regional affiliates. Pure cargo carriers, such as FedEx and UPS Airlines, were not included. Airlines are assigned to specific categories each year based upon an assessment of a carrier’s ancillary revenue profile.

(2) IATA Economy Performance of the Airline Industry, 2018 Mid-Year Report (amount includes airline revenue and indirect taxes)

Theodore is the Co-Founder and Managing Editor of TravelDailyNews Media Network; his responsibilities include business development and planning for TravelDailyNews long-term opportunities.