AirDNA’s latest report on the European short-term rental market reveals strong growth in demand and changing trends in seasonality, with February 2023 seeing a 47.3% increase compared to the same period in 2019, and 26.6% higher than last year, despite being a typically low demand period.

Typically considered a low demand period, European short-term rental demand in February was 47.3% higher than the same period in 2019 (26.6% higher than in 2022 and 115.9% higher than in 2021). Marking the second consecutive month of growth, available listings rose by 2.8% relative to 2019, otherwise increasing by 13.7% from 2022. Despite such a significant gap in demand and listing growth, the number of available listing nights has increased steadily in line with demand as hosts open up their calendars for longer periods. In February, the supply of available nights was 37.8% greater than in February 2019 (20.7% vs. 2022).

However, available listing night growth was slow in comparison to demand growth during this off-peak month, which led to a 6.9% increase in occupancy levels relative to 2019 (4.9% vs. 2022). The rise in demand also led to a 13.7% increase in average daily rates (ADRs) year over year, which pushed revenue to a record high of $3.7 billion in February, representing a 43.9% year-over-year (YoY) increase, 112.5% higher than in 2019. Accordingly, RevPAR in Europe was up by 19.2% compared to the previous year, a reflection of the increase in rates and occupancy.

At a Glance: Key European STR Performance Metrics for February 2023:

- RevPAR rose by 19.2% YoY

- Available listings held strong, 2.8% above 2019, 13.7% YoY

- Total demand (nights) was 47.3% higher than 2019, 26.6% YoY

- Occupancy up 6.9% vs. 2019, +4.9% vs. 2022

- Average daily rates (ADRs) up 13.7% YoY

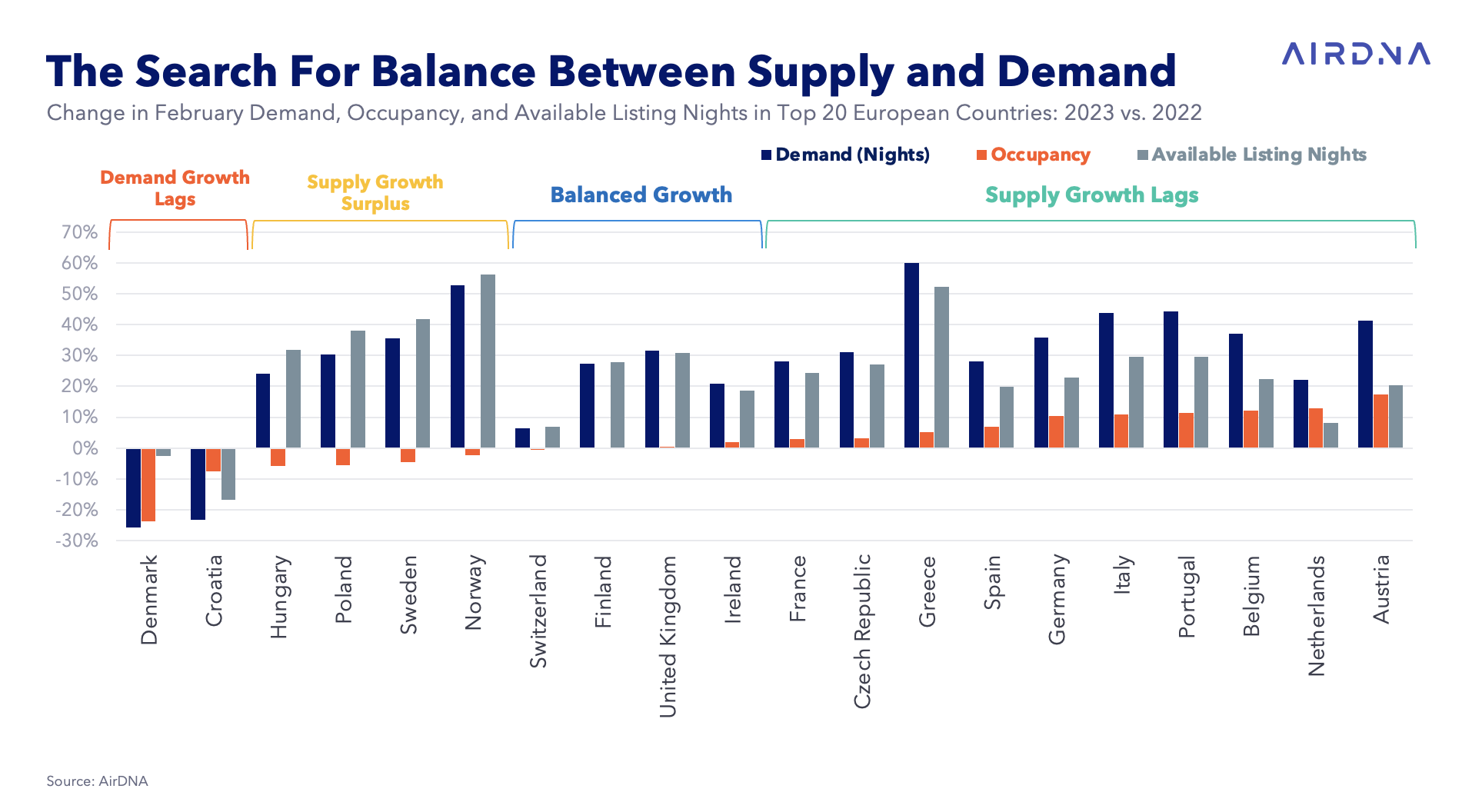

Top 20 Countries Search for Balanced Occupancy Levels

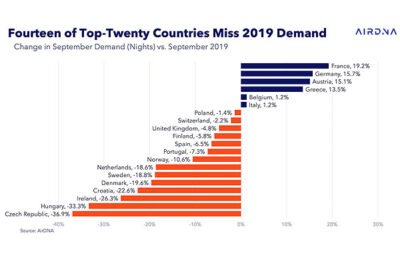

Short-term rental demand and supply trends in Europe varied across countries during what is historically the least busy period of the year. In February, Greece, Norway, and Portugal experienced the highest growth rates in demand, with year-over-year increases of 60%, 52.7%, and 44.1%, respectively, showcasing a strong appetite for short-term rentals in these destinations. In terms of supply, the largest increases in available listings over last year were seen in Norway, Sweden, and Poland (up 54.2%, 36.7%, and 35.9%, respectively), indicating a willingness by hosts to meet the demand. Interestingly, Croatia experienced the highest growth in ADR (30.8%), despite a significant decline in available listings (-14.1%), suggesting a changing market landscape and broader economic pressures as demand in the nation fails to keep pace with last year (-23.2%).

Occupancy levels in the top 20 European countries faced a challenge in February due to contrasting off-season growth in demand nights and available listing nights. Excessive growth in either of these metrics during a low period such as February can throw occupancy off kilter, and hosts should be diligent to recognize the underlying opportunities that changing trends in seasonality can bring.

To analyze this, we divided the countries into four groups based on their growth rates: those where demand growth lags; those with a supply growth surplus; those with balanced growth; and those where supply growth lags. Switzerland, Finland, the United Kingdom, and Ireland achieved balanced occupancy levels, where available listing night supply growth and demand growth were on par with each other. On the other hand, Hungary, Poland, Sweden, and Norway saw growth in demand, but their occupancy levels declined as the supply of available listing nights grew at a greater rate than nights booked, putting them in the supply growth surplus category. On the supply growth lags end of the spectrum, Austria, the Netherlands, and Belgium experienced the steepest increases in occupancy levels, with growth rates of 17.4%, 12.9%, and 12%, respectively. Demand growth exceeded supply growth in these markets, leading to sharp increases in occupancy and signaling an opportunity to service unmet demand with additional available listing night supply. Occupancy was the steepest to fall in Denmark, with a decrease of 25.7% year over year, while Croatia also saw a notable decline of 7.7%. These two countries continued to experience a lag in demand growth, justifying the decline in available listing nights figures and, ultimately, occupancy declines.

Impact of Regulatory Changes in Addressing Affordability

In February, Ireland and Portugal ended their respective Golden Visa programs, which granted non-EU nationals the opportunity to acquire EU residence through financial investment in the countries. Following suit, Spain may be the next country to end the program as Congress there mulls over a bill submitted last month which would eliminate the possibility of obtaining a Golden Visa by purchasing real estate in Spain. The decision to terminate the visa program has been attributed to concerns over rising real estate speculation, an issue to which short-term rentals are often erroneously cited as a key contributor.

Many markets have attempted to tackle the issue of housing affordability through the implementation of stringent short-term rental regulations. However, this approach may be misguided, as broad price increases have been seen across the European real estate market. According to Eurostat data, the increase in home prices has been consistent since 2015. The rise in property values has affected all types of properties in the Euro Area, but the increase has been lesser among owner-occupied units—those where the owner is using the property as their own primary dwelling—relative to the broader market. Growth in house prices in other types of property—including those destined for second homes or rentals—has been higher. This calls into question the effectiveness of short-term rental regulations in addressing the root causes of rising home prices in the Euro area.

Homes which are not occupied by the owner commonly fall under the category of a second home or investment property. Often leveraged as cash-flowing assets, these types of properties are not easily comparable to traditional long-term housing, as they cater to a different market segment and offer a different set of amenities and services. The rise in home prices since the pandemic can be attributed to a broad increase in demand and mounting inflationary pressures across the real estate industry. The price increases in non-owner-occupied properties have a propensity to be more dramatic than the broader real estate market and tend to be confined to higher-tiered units and upscale renters. This is further supported by the fact that short-term rental RevPAR has increased at the greatest rate among higher-end units since 2019. In February, among entire homes and apartments, RevPAR relative to the same month in 2019 had increased by 52.3% for luxury units, 40.4% for upscale units, 37.3% for midscale units, 33.7% for economy units, and 24.4% for budget units.

The largest cities in a country are often the first to implement regulation in a myopic effort to tackle housing affordability. With tourism in urban areas having been hardest hit since the pandemic, both short-term rental demand and supply have been severely impacted, and many of these areas are yet to recover to 2019 levels. Short-term rentals provide revenue streams for hosts and nearby businesses, generate tax revenue for local governments, and create job opportunities for the community. For urban markets faced with a new set of regulations, a full recovery may not even be within the realm of possibility, rendering an economic loss to the community of all of the benefits that short-term rentals provide. In February 2023, available listings in Europe’s top 50 cities remained 22.8% below 2019 figures, while demand lingered 13.1% lower in the same period. Notably, this was the best month yet for the largest markets compared to pre-pandemic periods, and recovery has been slow and steady. But the prolonged vacuum of demand has dealt a significant blow to short-term rental operators in many urban tourist destinations. Having been hit hard in their pocketbooks, many operators in the top 50 markets have chosen to repurpose their properties for long-term rentals or move to a new market entirely.

On the flip side, further investment is being seen outside of urban areas, many of which have experienced substantial growth in tourism figures in the last three years. Short-term rentals are a driving economic force that bolsters the existing forms of accommodation through alternate offerings that would otherwise not exist. European markets outside of the top 50 saw a 63.4% rise in demand compared to pre-pandemic levels in February, while available listings have increased by 8.8% during the same period. This presents an opportunity for further investment in these areas, and an increase in barriers to entry could hinder economic growth in regions that benefit from it the most.

Despite contrasting levels of growth in demand and supply between the top 50 markets and everywhere else in Europe, unit-level occupancy has been able to make progress across both focus areas over the last year. That is to say that the number of the nights available in the top 50 markets and everywhere else has been just below adequate to satisfy demand, leading occupancy growth relative to pre-pandemic periods. In February 2023, occupancy in the top 50 markets was 5.8% above 2019 levels and 10.1% higher in markets everywhere else. On the whole, over the last year, occupancy growth has been greatest among markets outside of the top 50, but of the listings that are available in the top 50, a moderate growth in occupancy is being experienced relative to 2019.

When isolating the focus to changes in short-term rental supply and demand in Ireland, Portugal, and Spain, we conducted a comparison between the top five largest markets and those outside of these. By comparing total annual data from 2022 to 2019, we can see that both demand and supply in the top five markets of each of the three countries were slower to recover compared to other areas. Interestingly, Portugal and Spain were able to increase demand figures in areas outside of their top five largest markets, with growth rates of 11% and 3.4%, respectively. Although demand outside of the top five markets in Ireland remained lower than in 2019, these areas performed better than the top five largest markets. Supply growth relative to pre-pandemic levels remained stunted across the focus countries, irrespective of market size. However, the markets outside of the top five markets in Portugal, Ireland, and Spain fared better in the period, down by 6.9%, 19.8%, and 7.3%, respectively. Meanwhile, available listings in the top five markets had been leveled in Portugal by 21.1%, Ireland by 48.1%, and Spain by 28.9%.

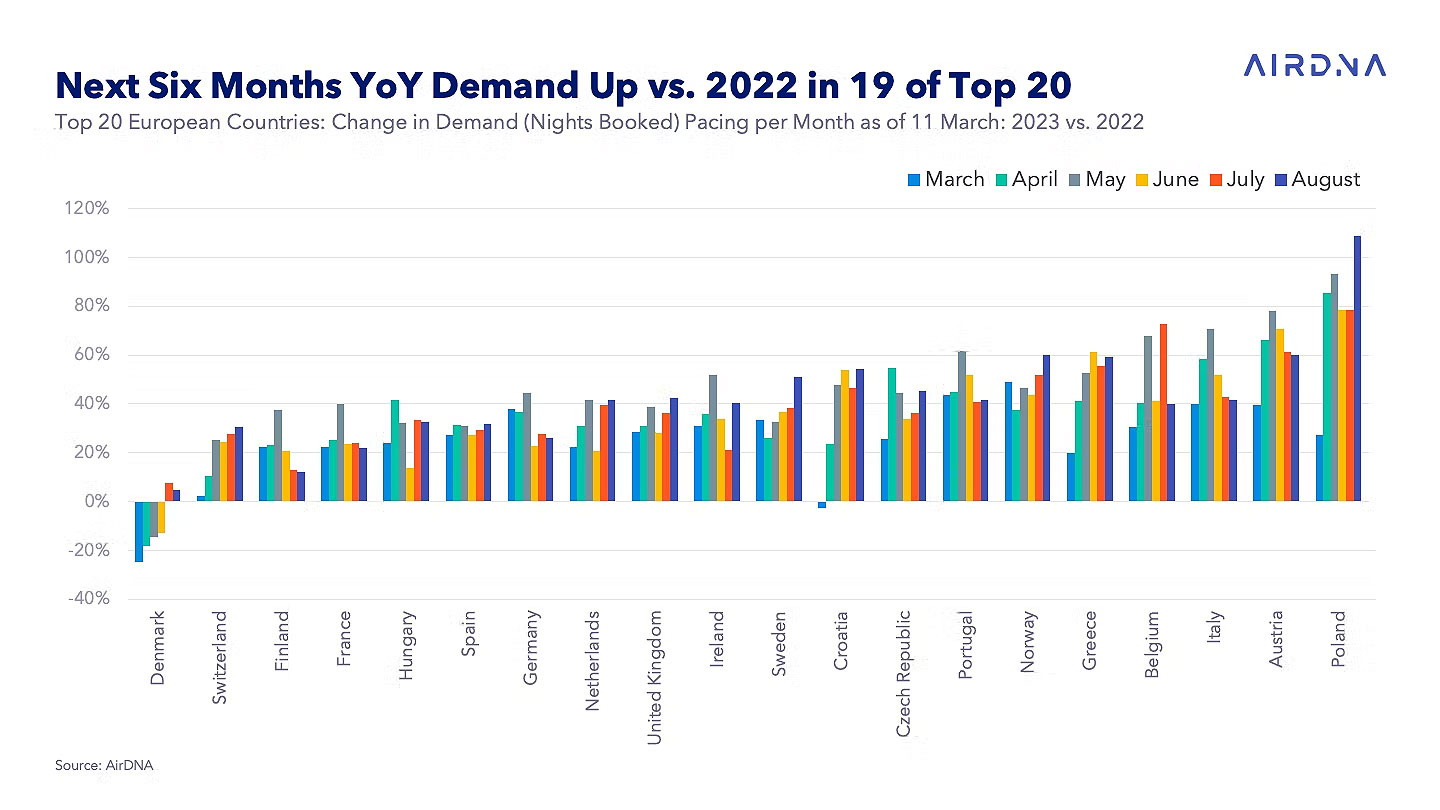

Growth Continues Into Summer

Demand pacing trends indicate that growth and momentum within the European short-term rental industry are set to continue over the next six months. As of March 11th, the continent was tracking record-setting demand pacing over the next six months, up by an impressive 32.8% year over year and 24.5% compared to 2019. May was the standout month, with nights booked pacing 42.6% higher than in 2019 and 42.5% higher than in 2022. With May typically considered a less busy month for tourism after the Easter break, this signals that travel seasonality is expanding beyond peak periods. That said, travelers remain eager to lock in their summer accommodations. As for the months of June, July, and August, nights booked were pacing up by 32.3%, 33.7%, and 34.9%, respectively, over 2019.

A closer examination of the top 20 countries in Europe reveals similar trends in nights booked. The month of May saw the greatest year-over-year change in demand pacing within the next six months in Austria, Italy, Portugal, Ireland, the Netherlands, Germany, France, and Finland. What’s more, all but one of the top 20 countries (Denmark) were trending toward double-digit growth in total nights booked between March and August. Poland, Austria, and Italy were leading the way in growth, with total nights booked over the next six months up by 65.6%, 58.6%, and 50.0%, respectively. These trends bode well for the European short-term rental industry, with travelers showing a keen interest in exploring the continent’s diverse cities and landscapes throughout the year.

Tatiana is the news coordinator for TravelDailyNews Media Network (traveldailynews.gr, traveldailynews.com and traveldailynews.asia). Her role includes monitoring the hundreds of news sources of TravelDailyNews Media Network and skimming the most important according to our strategy.

She holds a Bachelor's degree in Communication & Mass Media from Panteion University of Political & Social Studies of Athens and she has been editor and editor-in-chief in various economic magazines and newspapers.